Impact Analysis of Climate Change-Related Risk

The risks of climate change can be divided into transition risks and physical risks.

Transition risk refers to the risk that occurs in transitioning to a society with low greenhouse gas emissions (a low-carbon society). For example, the introduction of a carbon tax levied on greenhouse gas emissions could lead to a negative financial impact on investees and borrowers that have high emissions. This in turn could result in credit costs for financial institutions.

Physical risks are risks of intensification or increase in extreme weather events due to climate change or from long-term changes in climate patterns. Physical risks can be classified further into acute risks, such as increased flooding or other extreme weather events, and chronic risks, such as the agricultural impact of prolonged high temperatures.

Climate Change Risks Recognized by the Bank

| Risk | Classification | Major Risks | Time Frame |

|---|---|---|---|

| Transition Risk | Government Policy, Legal, Technology, |

|

Mediumm to long term |

| Policy |

|

Short term | |

| Reputation |

|

Short term | |

| Physical Risk | Acute |

|

Short, Medium, and Long Term |

| Chronic |

|

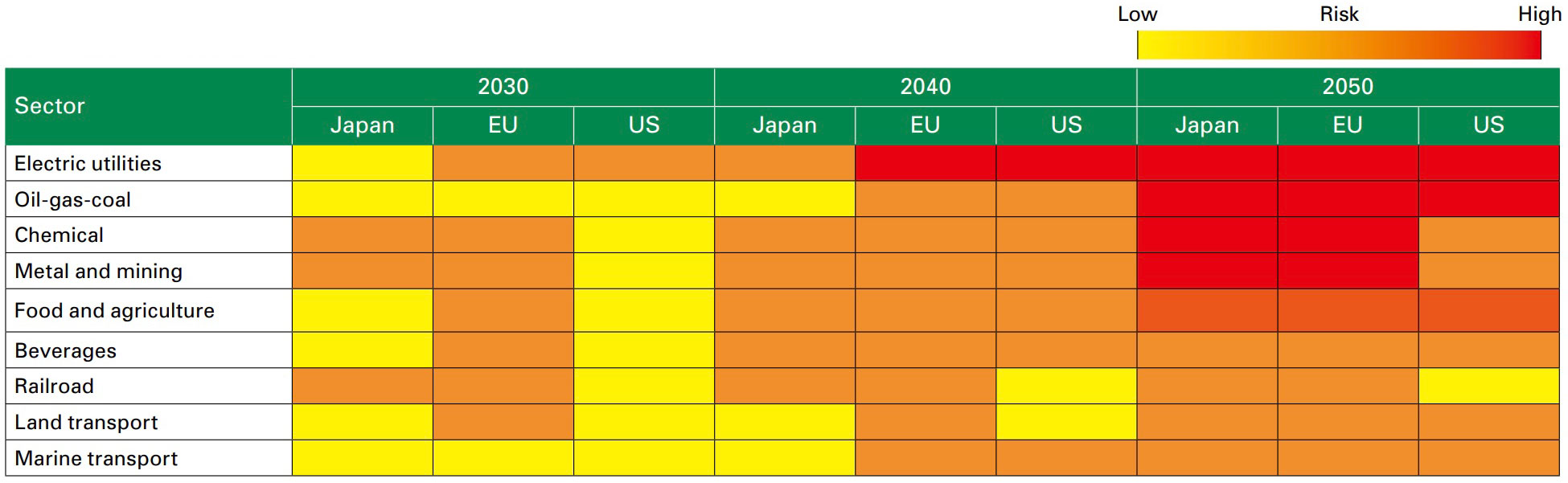

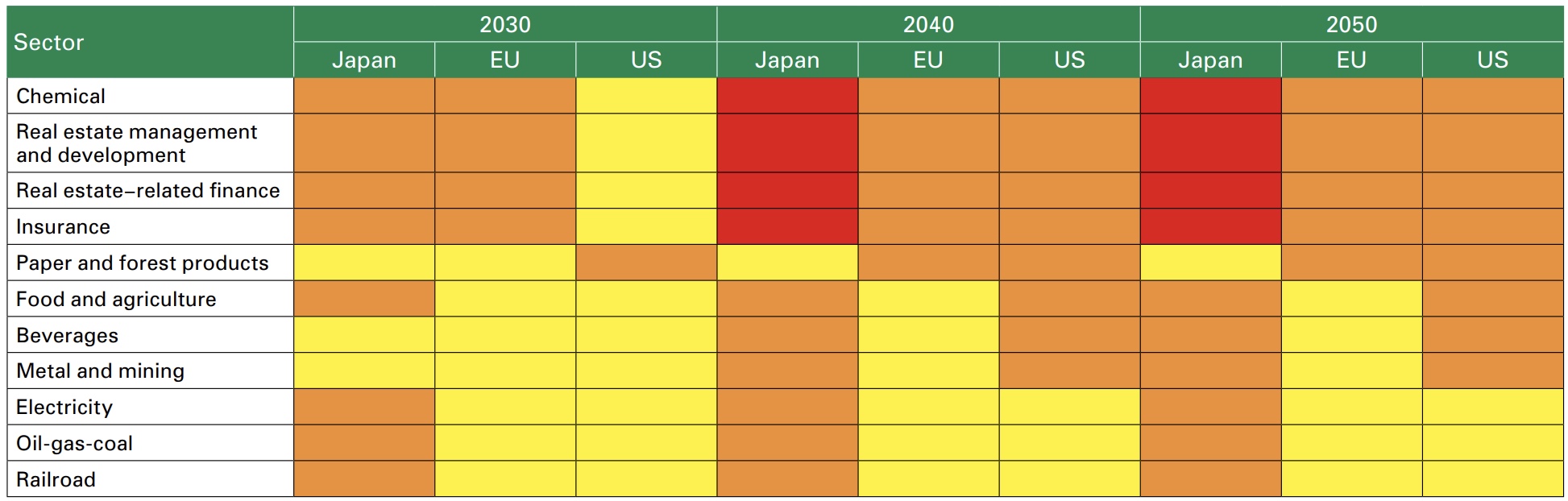

Climate Change-Related Risk Assessment by Sector

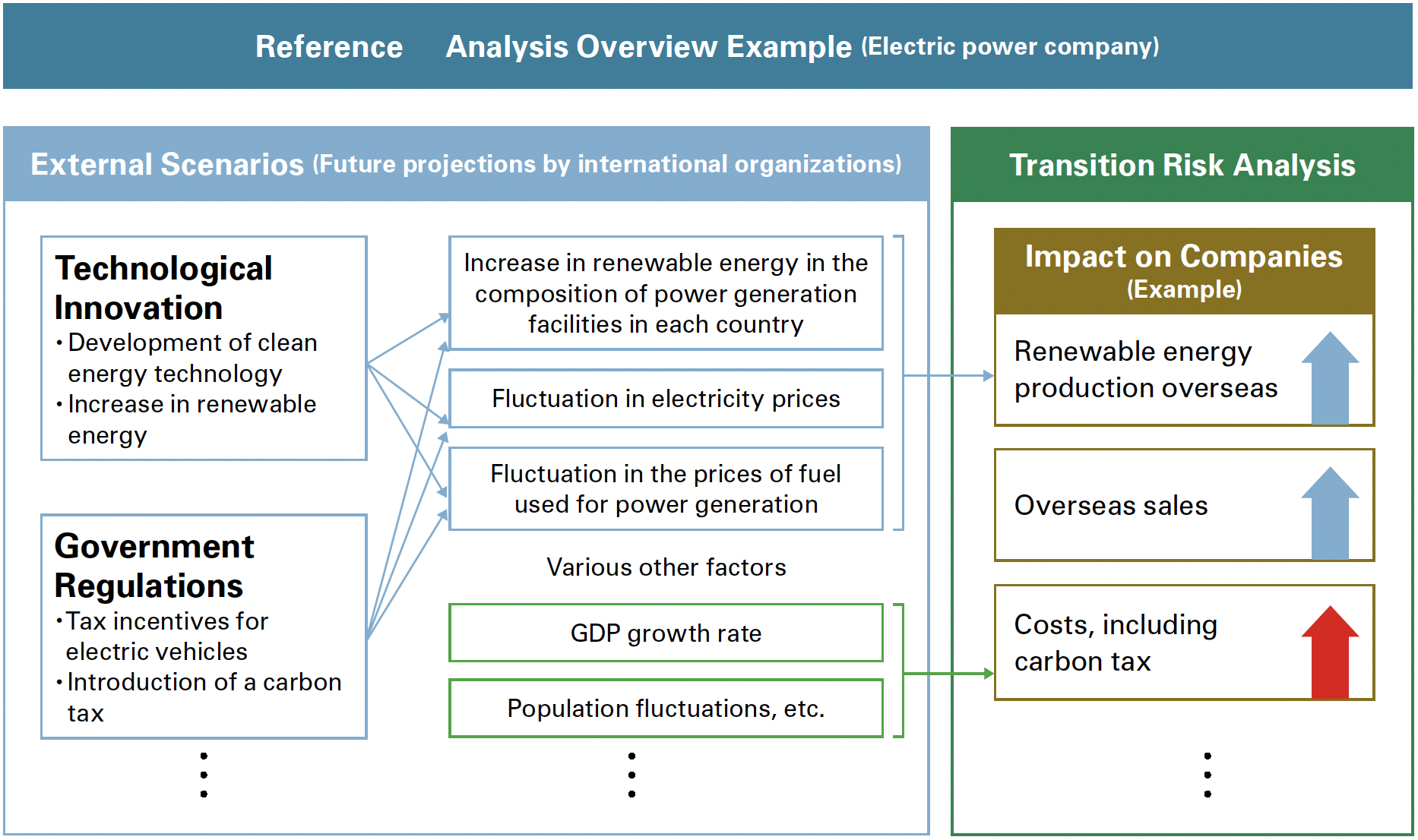

The impact of climate change will become even more apparent over the medium- to long-term, and will vary depending on the sector in which our investees and borrowers operate. Therefore, we evaluated where and when transition and physical risks would occur in the targeting sectors and other areas defined by the TCFD recommendations.

The occurrence of risks associated with climate change is caused by various external factors, environments, and spillover channels. We created the table below after identifying these risks and factors. The table shows (in chronological order) the impact of these risks on the sectors in which the Bank has most financial exposure. Our analysis also reflects the effects of climate change occurring at different times according to region, geographic conditions, and legal regulations. As one example, transition risks in the EU are expected to occur early due to environmental regulations being adopted ahead of the rest of the world.

Transition Risk Assessment*1

Physical Risk Assessment*1

- *1 Transition risks are assessed based on a 2°C scenario in which policy measures mitigate climate change, while physical risks are assessed based on a 4°C scenario in which global warming advances.

Impact Analysis of Climate Change-Related Risk (Scenario Analysis)

We conduct scenario analyses to understand the impact of climate-related risks on our credit Step 2 Step 3 portfolio and finances.

Transition Risk Scenario Analysis

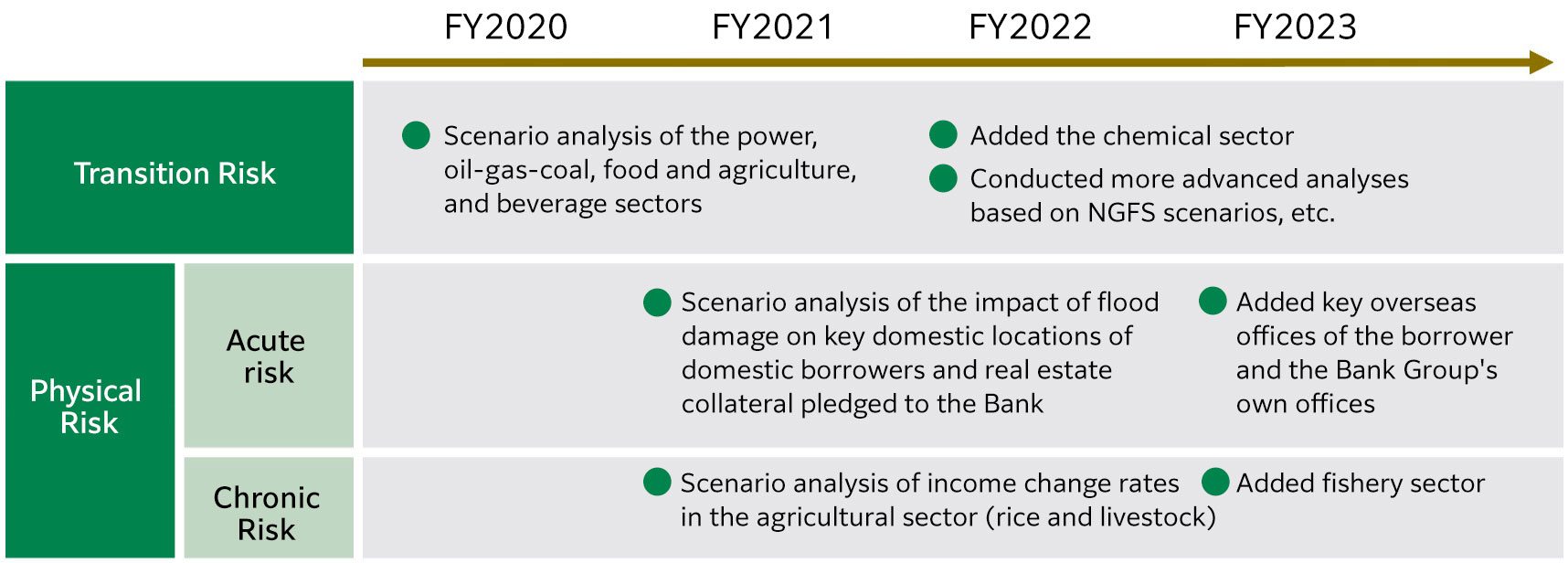

We selected target sectors for our transition risk scenario analysis based on our risk assessments on climate change intensive sectors. These sectors include the high-risk sectors of power, oil-gas-coal and chemicals, as well as the food and agriculture and beverages sectors, which form the food and agricultural value chains. Through scenario analysis for these sectors in fiscal 2022, we evaluated medium- and long-term changes in credit costs caused by the progress of decarbonization. In fiscal 2024, we began working to upgrade our analysis, as well as expanding our scope of analysis for the steel sector.

Scenarios analyzed include the Net Zero2050 scenario published by the Network of Financial Authorities on Climate Change Risk Network of Central Banks and Supervisors for Greening the Financial System (NGFS), as well as scenarios published by the leading International Energy Agency (IEA) etc.

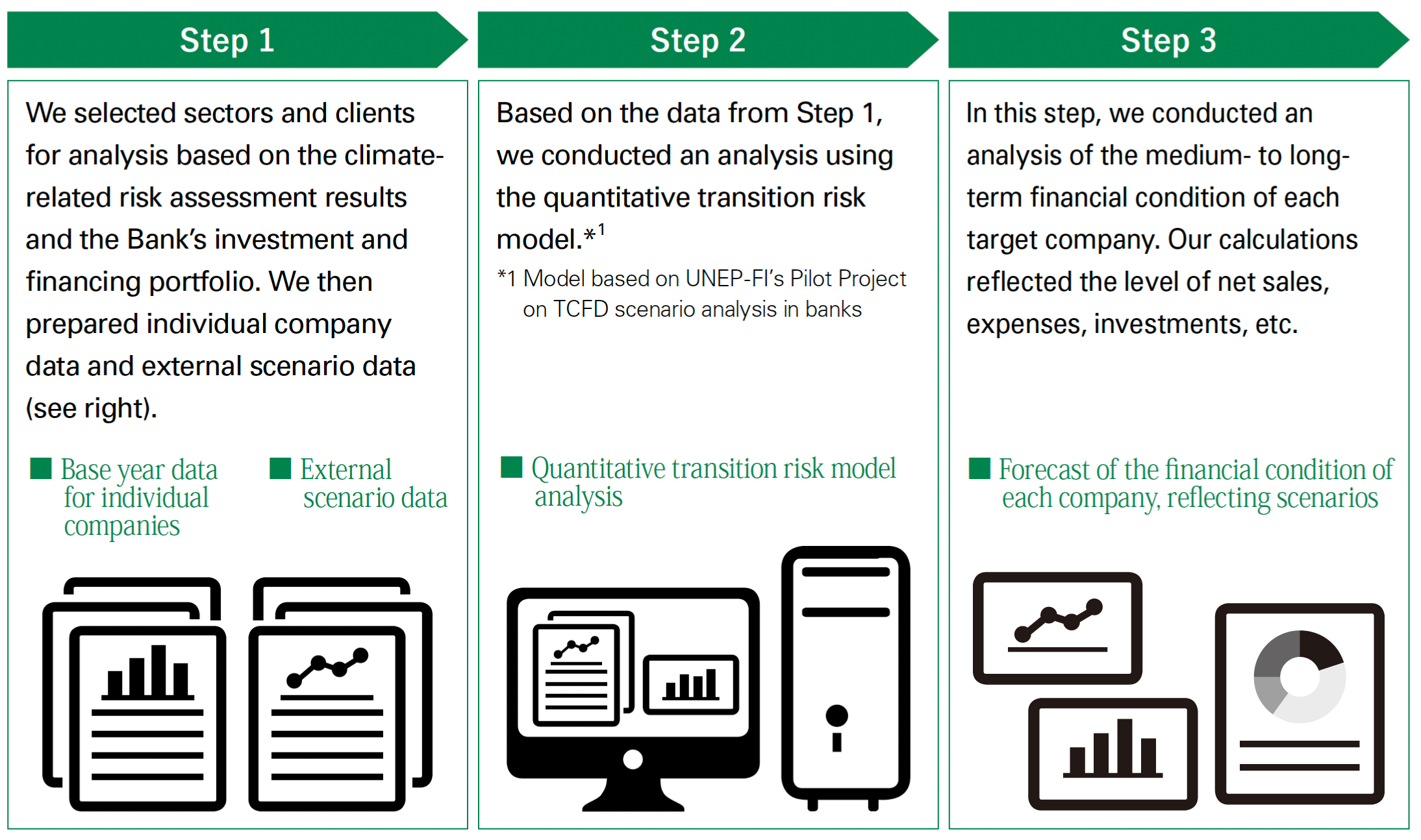

Our analysis was based on the method published by the pilot project led by the United Nations Environment Program Finance Initiative (UNEP FI) with the objective of discussing and developing methods for climate-related financial information disclosure in the banking industry.

Transition Risk

Methodology for Transition Risk Scenario Analysis

■ Targets and sectors analyzed

Based on the results of our qualitative assessment of climate change-related risks, we selected the electricity, oil-gas-coal, food and agriculture, beverages, chemicals and steel sectors as targets for transition risk scenario analysis. Power, oil-gas-coal, chemicals and steel sectors have been identified in the final TCFD report and SASB as sectors having high carbon emissions and highly vulnerable to transition risks. Our selection was based on initiatives consistent with these global views. We selected the food and agriculture and beverages sectors based on the results of our climate change qualitative assessment, as well as the fact that these two sectors form the foundation of the Bank. Given our investment and loan portfolio, the analysis covers not only domestic and overseas borrowers, but also our investees in corporate bonds.

■ Analysis scenario data

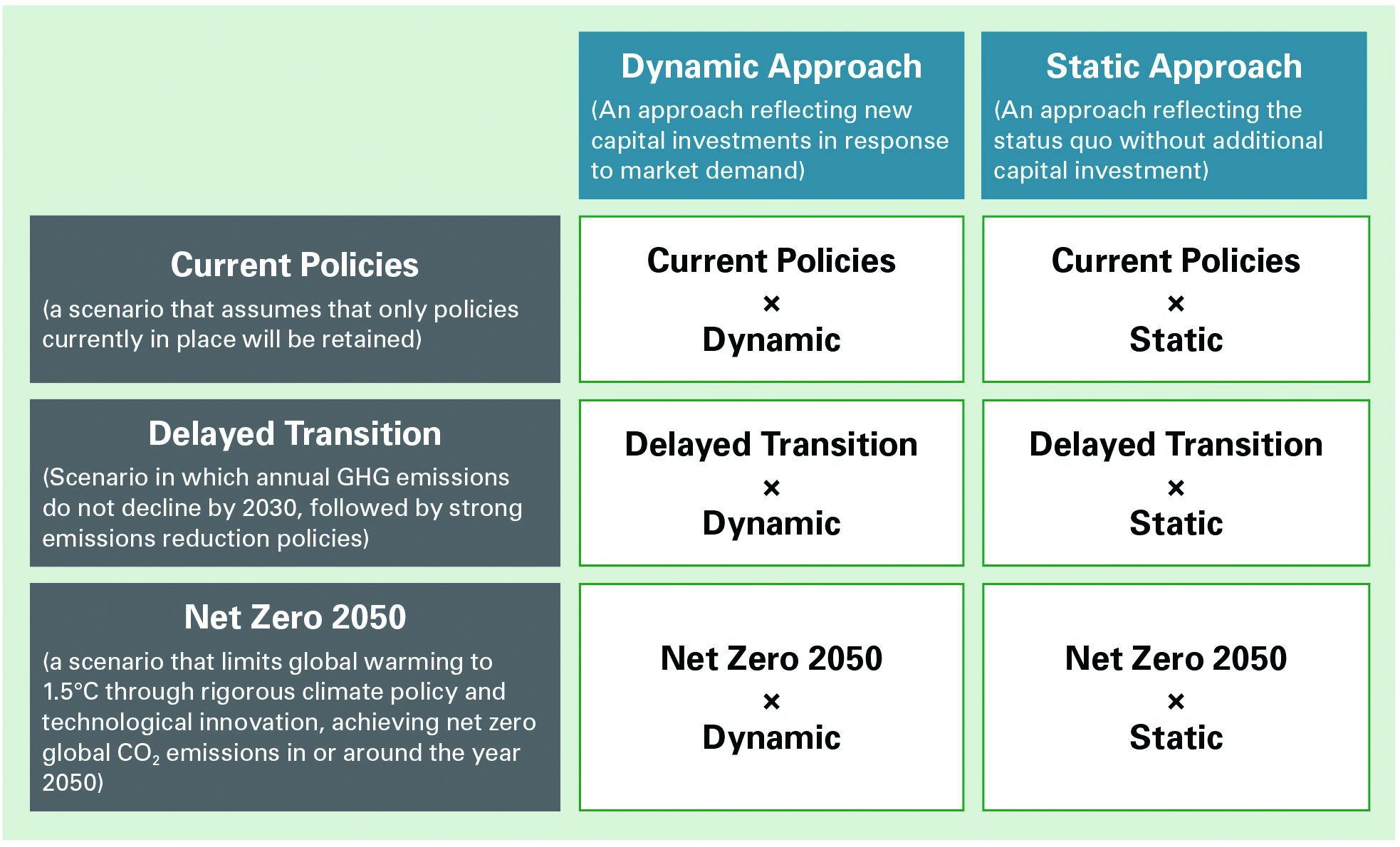

We use three scenarios published by the NGFS. Specifically, we adopted three future scenarios for our analysis. We used the Current Policies scenario, which assumes that only the policies currently in place are maintained, and the assumption that annual greenhouse gas (GHG) emissions will not decrease by the year 2030. We then used the Delayed Transition scenario, in which strong policies are implemented to limit global warming to 1.5°C through rigorous climate policy and technological innovation. And last, we used the Net Zero 2050 scenario, which assumes net zero global CO₂ emissions will be achieved in or around the year 2050. We predicted the impact on the Bank’s investees and borrowers , while also analyzing the increase or decrease in credit costs. We formed our predictions by combining the Dynamic approach, in which companies make new capital investments in response to climate change, and the Static approach, in which companies do not make additional capital investments in response to climate change.

- In connection with the NGFS scenario for which we lacked sufficient data, our analysis used as complementary data from IEA, WRI (World Resources Institute) etc.

- In connection with the analysis of the chemical sector, we referred in part to the IEA’s World Energy Outlook 2023.

- In connection with the steel sector, we partially referred to the data contained in the IEA World Energy Outlook 2023 and the IEA Iron and Steel technology Roadmap.

- For the food and agriculture and beverage sectors, we used WRI data as complementary data.

■ Efforts to increase the sophistication of scenario analysis models

- We began disclosing the results of our scenario analysis with our Sustainability Report 2021. We also strive to improve the sophistication of our models to utilize analysis results to better explanation of our position and conducting engagement (constructive dialogue).

- As an example, we made improvements by replacing parameters (variables) in the analysis model to make the analysis results more precise and consistent with real-world perspectives. We will continue to refine the results of our analysis by upgrading our models as necessary.

| Analysis Target | Selection Scenario | Complementary Scenario |

|---|---|---|

| Energy (Electricity, Oil-Gas- Coal) |

NGFS

|

|

| Food and agriculture, beverages | WRI CREATING A SUSTAINABLE FOOD FUTURE: FINAL REPORT, JULY 2019 | |

| Chemicals | IEA Energy Technology Perspectives 2022ーSTEP、SSDS IEA Ammonia Technology Roadmap October 2021 ーSTEPS、SDS |

|

| Steel | IEA World Energy Outlook 2023 and the IEA Iron and Steel technology Roadmap |

Six-Way Scenario Analysis

About the NGFS Scenario Used in Analysis

- Our transition risk scenario analysis adopts version 4 of the NGFS scenario published in 2023. Of the three NGFS models, we analyze scenarios using the values of the REMIND-MAgPIE model. These values were also used in the Pilot Scenario Analysis Exercise on Climate-Related Risks Based on Common Scenarios by the Financial Services Agency and the Bank of Japan, the results of which were published in August 2022.

Overview of NGFS Scenarios Analyzed

| NetZero 2050 | Delayed Transition | Current Policies | |

|---|---|---|---|

| Overview | Limits rise in global temperatures to 1.5°C through strict climate policies and technological innovation, reaching net zero CO₂ emissions by 2050 | Assumes annual CO₂ emissions will not decrease until 2030, followed by strict policies | Assumes that only current policies will be retained |

| Rise in temperature (by 2100) | Less than 1.5℃ | Approx. 1.8℃ | Approx. 3℃ |

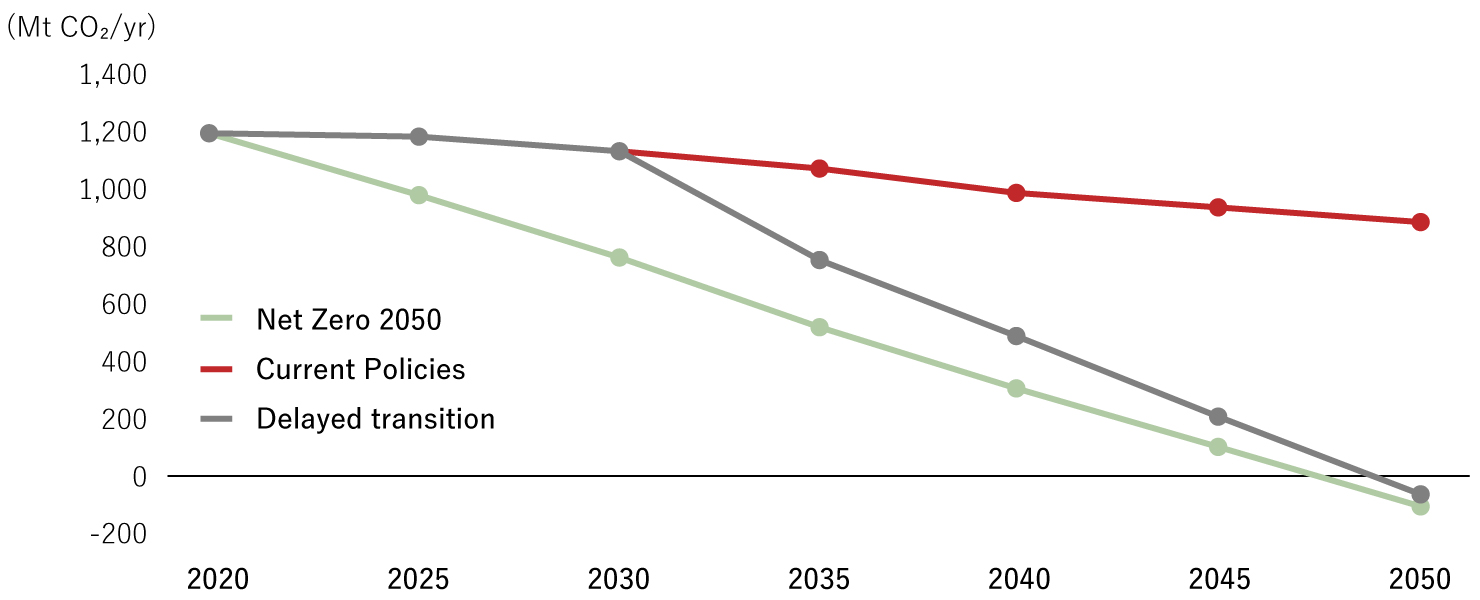

- Each NGFS scenario analyzes from different forecasted perspectives. The Net Zero 2050 scenario assumes that countries implement immediate, strict climate change policies and regulations, thereby reducing corporate CO₂ emissions. On the other hand, the Current Policies scenario assumes that CO₂ emissions will not be curbed, while the Delayed Transition scenario assumes rapid decline in CO₂ emissions starting in 2030 after implementation of strict measures and policies.

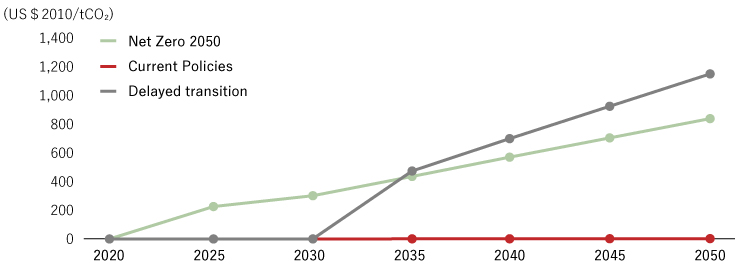

- A carbon price refer to the price assigned to CO₂ emitted from companies and others entities. Each scenario assumes that governments would impose taxes on carbon based on the amount of CO₂ emitted. For example, Japan introduced a restrictive carbon tax to address global warming, which the Current Policies scenario assumes will be maintained. While tax per ton of CO₂ emissions is assumed to be limited, the Net Zero 2050 and Delayed Transition scenarios assume significant introductions of carbon tax. The Bank assumes the introduction of a carbon tax in our scenario analysis, and we reflect impacts on corporate earnings and other factors in the analysis results.

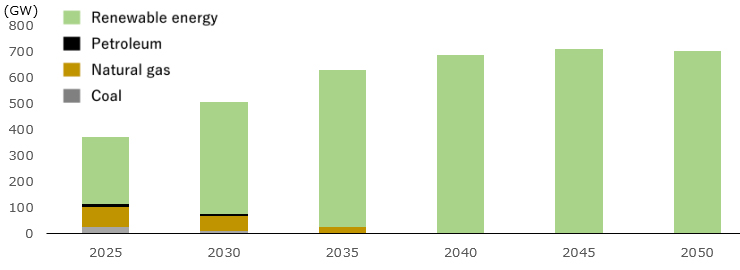

- The Net Zero 2050 and Delayed Transition scenarios aim for carbon neutrality by 2050. In these scenarios, solar power, wind power, and other renewable energy sources serve as the main energy sources to reduce CO₂ emissions. At the same time, power generation that emits large amounts of CO₂ using coal and natural gas is reduced in these scenarios.

CO2 emissions (Japan)

Carbon pricing (Japan)

Power generation capacity under the Net Zero 2050 Scenario (Japan)

Transition Risk Scenario Analysis Results

- Electricity and Oil-Gas-Coal Sectors

In every scenario, greater demand for renewable energy and stricter regulations on carbon emissions in various countries would result in stranded fossil fuels and reduced market demand. Business whose profits depend on fossil fuel prices will likely see declining performance. - Chemicals Sector

Results varied depending on the chemical products manufactured and the region in which the company operates. The Delayed Transition Scenario toward decarbonization and the Net Zero 2050 scenario resulted in slower economic growth. These scenarios revealed relatively lower demand for each chemical product compared to the Current Policies Scenario, with the exception of certain products. On the other hand, demand for hydrogen and ammonia as fuels that do not emit CO2 directly is likely to increase. Demand for functional chemical products used as battery materials is also likely to increase with the wider adoption of electric vehicles; however, price shifts to products should be limited in nature. - Steel sector

Results varied depending on business structure and the region in which the company operates. Carbon cost impacts differ significantly between individual companies under The Delayed Transition Scenario toward decarbonization and the Net Zero 2050 scenario depending on the amount of GHG emissions. Especially the companies that operate in the U.S. and in South-East Asia, where steel demand is expected to increase, capital investment to decarbonize the steel industry has led to an increase in earnings. - Impact on Credit Portfolio

The total impact of transition risk in the four aforementioned sectors could increase the cost of credit by between 1 billion yen to 25 billion yen per year through the year 2050. The impact on our credit portfolio would be limited.

Using Analysis Results

Based on the results of the transition risk analysis, we initiated dialogue on climate change initiatives with our investees and borrowers in sectors where we identified a relatively large impact. By sharing an awareness of the issues with our investees and borrowers, we will strengthen our efforts to address climate change together and work toward creating a lowcarbon and decarbonized society.

Scenario Analysis for Physical Risk Related to Climate Change (Acute Risk)

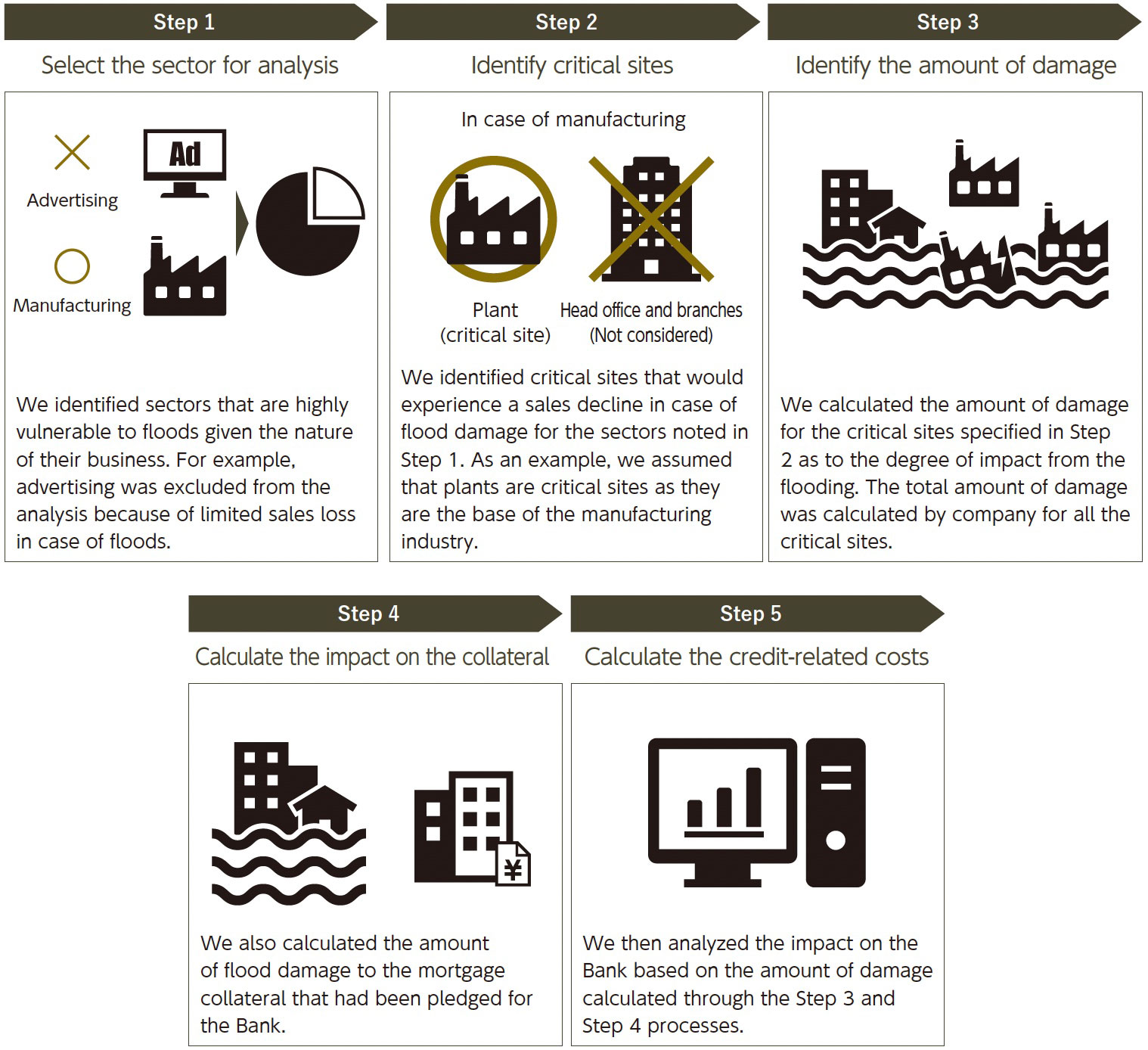

We analyzed acute risk related to flood damage, which has caused significant problems in recent years. In addition to key global locations of domestic and overseas borrowers and real estate collateral pledged to the Bank, we included the assets of Bank Group locations (buildings and equipment) in the analysis.

Our acute risk scenario analysis indicated a cumulative additional loss of about 23 billion yen (sum of credit costs and damage to the Norinchukin Bank Group assets) through the year 2100. The impact of additional losses would appear to be limited. See the Appendix for details.

Physical Risk (Acute Risk) and Scenario Analysis Overview

Physical Risk (Acute Risk) Analysis Overview

| Subject of Analysis | (1) Key domestic and overseas locations of borrowers expected to be affected by flooding (2) Real estate collateral pledged to the Bank (3) Assets at the Bank Group domestic and overseas locations (buildings and fixtures) |

|---|---|

| Not Subjected to Analysis | Industries where flood damage is not expected (e.g., advertising, publishing, finance, etc.) |

| Analysis Scenario | IPCC RCP2.6 and RCP8.5 |

| Measurement Results | Cumulative additional losses of approximately ¥23 billion through the year 2100 (credit costs plus damage to Bank Group assets) |

Using analysis results

For this analysis, we extended the scope of scenario analysis measurement to identify the additional cumulative losses through the year 2100 for which we must prepare. We will consider analyzing and measuring the impact of hazards other than flooding associated with physical risks. These analyses will take the supply chain into account, utilizing the information related to the borrower's key domestic and overseas locations surveyed in this analysis.

In addition, we plan to practice operational risk management for the high-risk assets owned by the Norinchukin Bank Group. We intend to engage our borrowers appropriately and work with them to step up their efforts in addressing climate change.

Physical Risk (Chronic Risk) Analysis

The Norinchukin Bank is committed to achieving Net Zero by 2050 across our investees and borrowers. In conjunction, we pursue an increase in the income of farmers, fishermen and foresters as a 2030 medium- to long-term goal in support of sustainable agriculture, fishery and forestry industries and local communities. Given that the agriculture, fishery and forestry industries are vulnerable to the effects of climate change, we endeavor to analyze the impact of climate change on the incomes of participants in these industries.

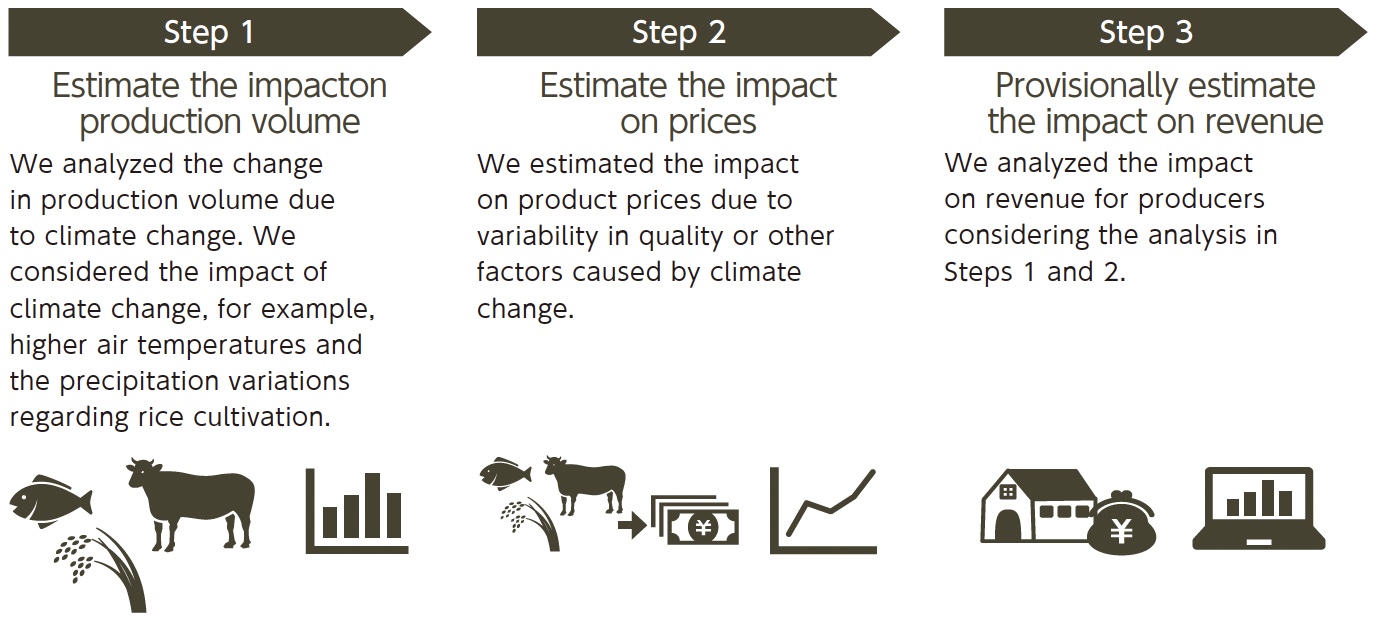

For chronic risk, we selected agriculture and fisheries as sectors to analyze. These industries are important to the Bank, which serves the agriculture, fishery and forestry industries. We chose rice cultivation, livestock production (raw milk and beef cattle), and ocean fisheries (bonito) as target commodities to analyze. Our analyses addressed the impact of climate change, including increases in air and ocean surface temperatures, on producer and fisher income, as well as adaptive measures.

This analysis estimated the change in revenue as of the end of the 21st century compared to the end of the 20th century in two scenarios: (1) one in which no measures are taken to adapt to rising temperatures and (2) one in which measures are taken to adapt to rising temperatures. We adopted the IPCC RCP 2.6 and RCP 8.5 scenarios (“2°C increase” and “4°C increase,” respectively) for analysis, conducting a total of four analyses.

Analysis method: Rate of change in production volume + Rate of change in product prices = Rate of change in revenue

The following provides a summary of the results of chronic risk analysis for the agricultural sector. The results indicate a decline in income due to the effects of climate change. However, it may be possible to achieve flat income levels through adaptive measures.

| Scenario | Production Volumes | Price | Income Without Adaptive Measures |

Income Introduction of Adaptative Measures |

|

|---|---|---|---|---|---|

| Rice Crop | 4°C rise | -6.4% | +1.4% | -5.0% | +3.5% |

| 2°C rise | +3.3% | -1.6% | +1.7% | ‐ | |

| Raw Milk | 4°C rise | -1.1% | +0.9% | -0.1% | ±0.0% |

| 2°C rise | -0.2% | +0.2% | ±0.0% | ‐ | |

| Beef Cattle | 4°C rise | -1.2% | +0.6% | -0.6% | ±0.0% |

| 2°C rise | -0.3% | +0.2% | -0.2% | ‐ |

The following provides a summary of the results of chronic risk analysis for the fisheries sector. The results indicate regional variances in income due to the effects of climate change. However, it may be possible to limit income declines through adaptive measures.

| Scenario | Production Volumes | Price | Income Without Adaptive Measures |

Income Introduction of Adaptative Measures |

|

|---|---|---|---|---|---|

| Ocean fishing (bonito) |

4°C rise | -9.2% ~+4.7% |

-0.6% ~+1.3% |

-8.0% ~+4.0% |

-7.6% ~+4.0% |

| 2°C rise | -9.2% ~+9.5% |

-1.2% ~+1.3% |

-8.0% ~+8.1% |

-6.1% ~+4.0% |

Our analysis includes several assumptions and hypotheses due to the many limitations in scenario analysis models for the agriculture and fisheries sectors. These limitations include 1) a lack of available methodologies established globally, 2) incomplete data, and 3) diversified and complicated impact channels. Note that impacts may differ from the actual impact on agriculture and fisheries management, as our analysis targets revenue, not income (i.e., the amount after deducting expenses, etc., from revenue).

- Sustainability

- Sustainability Management

- Highlights of Initiatives

- Formulation of Purpose of the Bank and Milestones of Sustainable Management

- Philosophies and Policies

- Sustainability Promotion Structure

- Sustainability Advisory Board

- Important Issues to Achieve Our Purpose

- Stakeholder Engagement

- Participation in Initiatives

- Sustainable Finance

- Initiatives for Creating and Visualizing Impact

- Initiatives to Manage Environmental and Social Risks

- Agriculture, Fishery, Forestry Industries, and Regions

- Environment

- Social

- Governance

- Report/Index