Initiatives for Compliance

Basic Compliance Policies

To fulfill its basic mission and social responsibilities and prove itself worthy of its customers’ and members’ trust and expectations, the Bank manages its business in accordance with societal norms, for instance, by fully complying with laws and regulations based on the principle of total self-reliance. We are also constantly working to achieve a higher degree of transparency by emphasizing proper disclosure and accountability.

As part of this effort, the Bank has defined its basic compliance policy in its Code of Ethics, Environmental Policy, and Human Rights Policy. In addition, the Bank disseminates the Code of Conduct to all officers and employees to show the criteria for judgment and action to ensure good faith and fair execution of duties as a prerequisite for business operations and advises specific ways of thinking to put the Shared Values into action. These measures will ensure that compliance awareness is thoroughly understood and practiced by all officers and employees as they go about their daily business.

In addition, internal audits are conducted regularly concerning the adequacy of the Bank’s efforts, including those to ensure compliance and to instill a sound risk culture. In response to recent growing societal demand for greater customer protection, based on its Customer Protection Management Policy, the Bank has taken steps to reinforce its management systems as part of its compliance efforts aimed at winning customer trust. These steps include providing explanations to customers, handling customer complaints and inquiries, managing customer information, managing contractors in the case of outsourcing customer-related business, and managing transactions that might involve a conflict of interest with customers.

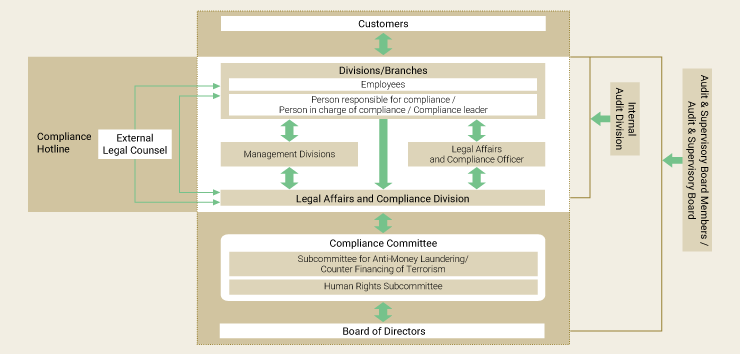

Compliance Activities Directly Linked to Management

The Bank’s compliance framework comprises the Compliance Committee, the Compliance Division (Legal Affairs and Compliance Division), and Legal Affairs and Compliance Officer, as well as personnel responsible for compliance, those in charge of compliance, and compliance leaders assigned to the Bank’s divisions and branches. The Compliance Committee has been established as a body under the Board of Directors to discuss and determine important matters pertaining to the establishment of the Bank’s compliance framework. Important matters discussed by the Compliance Committee and proposals thereof are subsequently approved by or reported to the Board of Directors. The Compliance Committee also treats operational risks, measures against money laundering and terrorist financing, and information security as agenda items, and discusses important policies for executing business pertaining to these topics.

In addition, the Subcommittee for Anti-Money Laundering / Counter Financing of Terrorism and the Human Rights Subcommittee, which are subcommittees under the Compliance Committee, are working to enhance discussions on the compliance framework and strengthen the PDCA cycle pertaining to the operation of the framework.

The Bank also has clarified its efforts to disseminate a sound risk culture and systematically prevent inappropriate behavior as part of its risk handling policy in the RAF.

Compliance Framework

Compliance Practices within the Bank

The Bank’s compliance framework at branches and divisions is based on the combined efforts of each employee, primarily centered on the General Manager of each branch or division and other equivalent persons who are responsible for compliance, together with a person in charge of compliance and a compliance leader. Directly appointed by the General Manager of the Legal Affairs and Compliance Division, persons in charge of compliance oversee all compliance-related matters at their branches or divisions. They are expected to handle requests for advice or questions from other members of staff, to organize branch or divisional training and educational programs, and to liaise with, report to, and handle requests to the Legal Affairs and Compliance Division.

Legal Affairs and Compliance Officers appointed in the Food & Agri Banking Business, the Retail Banking Business, the Global Investment and Banking, and the Corporate & Shared Services headquarters support each headquarters’ operations from the aspect of compliance.

The Legal Affairs and Compliance Division, supervising overall compliance activities, acts as the secretariat for the Compliance Committee. It strives to strengthen the compliance framework by conducting compliance reviews, responding to requests from branches and divisions for compliance-related advice, and conducting compliance monitoring, which includes visiting branches and divisions to verify their compliance practices directly while providing guidance.

Compliance Program

Each fiscal year, the Bank institutes a Compliance Program incorporating its management frameworks for compliance and customer protection, as well as promotion of initiatives, education, and training plans for them. The Legal Affairs and Compliance Division implements the Compliance Program and monitors its progress to further reinforce the Bank’s compliance framework.

Cooperation with Group Companies

To foster and disseminate a sound risk culture throughout the Norinchukin Group, the Bank shares its Code of Conduct with major group companies and provides support for its dissemination and translation to action at each. The Bank is taking steps to strengthen the compliance systems of the entire Norinchukin Group by promoting a common awareness of compliance issues discussed at regular meetings with compliance divisions of its group companies and providing support for formulating and implementing compliance programs and training activities at each group company. Additionally, to reduce compliance risks in the Norinchukin Group, the Bank has established an external contact for consultation on harassment, conducts offsite monitoring at each company (onsite monitoring at some companies), and takes other steps to identify problems as soon as possible.

Whistleblowing System

The Bank has established a whistleblowing system and put in place a Compliance Hotline so that if compliance problems occur, directors, employees, and others can report these either by phone or e-mail.

The Compliance Hotline offers several contacts to report to the Legal Affairs and Compliance Division or outside lawyers while enabling the reporter to choose anonymity or non-anonymity. When an issue is reported to the division, the Bank conducts an investigation, makes necessary improvements, and implements corrective measures. The Bank’s compliance operation prioritizes protecting whistle-blowers, for example prohibiting disadvantageous treatment of a whistle-blower and keeping the information of reported content secret, and the Bank makes efforts while striving to improve trust in the system.

In fiscal 2024, although ten cases were reported to the internal and external reporting channels at the Bank, none resulted in a major impact on the management of the Bank.

Notably, each overseas branch has contacts separate from those described above in place to receive reports from employees.

Measures to Prevent Money Laundering

The Bank has established policies to prevent money laundering as follows to ensure that the entire group complies with the relevant laws and regulations and fulfills its sound financial intermediary function.

Group-wide Basic Policy

The Bank and the Norinchukin Group comply with all applicable laws and regulations, take robust confirmation measures when accepting customers to exclude antisocial elements, terrorists, etc., and implement continuous customer management measures based on a risk-based approach. The Bank ensures the maintenance of its effective management system to prevent money laundering, in accordance with the characteristics of the Bank and the Norinchukin Group.

Customer Management Policy

With an appropriate internal system to prevent money laundering and other risks, the Bank takes the following measures according to the risk-based approach.

- Strict confirmation before each transaction using various information gathered when accepting customers initially, and the preservation of confirmation records

- Management measures to reduce money laundering and other risks, such as monitoring of transactions based on business characteristics, notification of suspicious transactions, and analysis and management thereof

- Control measures in accordance with the magnitude of money laundering and other risks for each customer, such as strict control of additional confirmation for customers with high money laundering and other risks

- Review of customer management measures based on the results of periodic investigation and analysis of all customer transactions

- Measures such as terminating transactions if appropriate customer management cannot be implemented or for other reasons

- Measures such as freezing assets of terrorists

- Prevention of economic sanctions violations

- Appropriate response to various regulations

- Confirmation of the anti-money laundering measures within foreign banks with which the Bank concludes correspondent agreements

- Continuous management and review of the above measures

Internal Management System Policy

The Bank takes the following measures to improve its internal management system to prevent money laundering and other risks.

- Establish and implement policies, procedures and plans for the prevention of money laundering and other risks; inspect and verify the status of compliance; and continually improve the system based on the results of such inspection and verification

- Promote all directors and employees awareness of the importance of their roles in preventing money laundering and other risks and foster a corporate culture of such awareness, through guidance and trainings

- Appoint managers in charge

- Clarify the roles of the divisions such as business divisions/branches that handle customers, operation management divisions, and audit divisions

- Report to the management on the status of measures to improve the management system over the entire Norinchukin Group, including its overseas offices; the status of customer management and other updates; and continue improvement measures

- Other necessary measures

Measures to Combat Bank Transfer Fraud

The Bank has established policies to prevent money laundering and other fraudulent activities and is strengthening preventive measures in this area as part of an increasingly necessary international cooperative effort.

Measures to Eliminate Antisocial Elements

Under the Code of Ethics, the Bank takes a strong and resolute stance against antisocial elements that pose a threat to social order and security, and in order to block all relationships with such antisocial elements, the Bank has established a systematic exclusionary system, in line with the following basic principles, and strives to ensure sound management.

(1) Response as an organization

The Bank has established the foundation of express provisions under the Code of Ethics and will respond as an entire organization, from the top management downward, and not simply leave it to the personnel or department in charge.

In addition, the Bank will guarantee the safety of employees who are asked to respond to unjustified demands from antisocial elements.

(2) Cooperation with outside agencies

In preparation for unjustified demands from antisocial elements, the Bank endeavors to establish continuing cooperation with outside agencies such as the police, the National Centers for Removal of Criminal Organizations and lawyers.

(3) Blocking of relationships including business transactions

The Bank shall block all relationships with antisocial elements including business relationships. In addition, unjustified demands from antisocial elements will be rejected.

(4)Civil and criminal legal responses in times of emergency

The Bank shall reject unjustified demands from antisocial elements and take legal action, if necessary, on both a civil and criminal basis.

(5) Prohibition of secret deals and provision of funds

Even in cases where the unjustified demands from antisocial elements are based on misconduct related to business activity or involving an employee, the Bank will absolutely not engage in secret deals. Furthermore, the Bank shall absolutely not provide funds to antisocial elements.

Bribery and Corruption Prevention

The Bank’s “Rules on Gift and Hospitality,” which are set forth under the Code of Conduct, clearly state that the Bank is committed to preventing corruption in all its forms, including extortion and bribery. Bribery includes the act of providing or offering to provide goods or other things (including non-monetary benefits) with the intention of influencing the recipient, and the act of accepting or requesting goods or other things with the intention of offering benefits to the provider.

In accordance with the said rules, the Bank stipulates the necessary procedures to ensure the appropriateness of gifts and hospitality acts involving the Bank or its directors and employees and ensures that all directors and employees are fully aware of these procedures. When those acts are conducted, the Bank ensures that the personnel responsible for and in charge of compliance confirm in advance that there are no problems from such perspectives as appropriateness and legal compliance.

In addition, the Legal Affairs and Compliance Division periodically monitors the status of gifts and hospitality acts and reports to the Compliance Officer, the Compliance Committee and the Board of Directors.

Moreover, the Compliance Hotline is in place to enable directors and employees to whistleblow on compliance issues, including corruption and bribery, by telephone or e-mail.

Information Security Initiatives

The Bank utilizes a variety of information obtained during transactions with customers, etc., for various kinds of operations. Amid the increasingly diverse environments and purposes for information handling due to the rapid progress and evolution of information technology, the Bank is focused on information security measures to protect and manage customers’ information appropriately.

The Bank’s Board of Directors has the ultimate responsibility for establishing and maintaining an information security management system. The Bank works systematically to enhance its information security, which is led by the Legal Affairs and Compliance Division with overall responsibility for information security planning, promotion, and progress management, together with the persons responsible for information security (General Managers) and other personnel in charge of information security of each branch or division. Also, important matters related to the improvement of the information security management frameworks are discussed mainly by the Compliance Committee.

Regarding the handling of personal information, the Bank has set out the Personal Information Protection Declaration and has established the security framework that complies with Japanese legal requirements as a Personal Information Handling Business Operator and Person in Charge of a Process Related to an Individual Number as defined under “Act on the Protection of Personal Information.” The Bank’s policy extends to suppliers (outsourcing contractors) to ensure their appropriate personal information management in case outsourced work involves personal information. Specifically, the Bank’s “Basic Policies for Risk Management” stipulates that processes and contractual relationships must be established to ensure the same level of risk management as if the Bank were performing the tasks internally.

The Bank conducts annual e-learning sessions for all employees on information security—including the appropriate handling of personal information—and also provides training at each level of the hierarchy to raise awareness of information security.

Overseas, the Bank has established a privacy policy applicable to the Bank’s London Branch and Norinchukin Bank Europe N.V., as well as a privacy policy for residents in the United States.

Responding to Customer Consultations and Complaints

The Bank takes consultations and complaints from customers seriously, responds to them promptly and systematically, and reflects them in its business operations in a positive manner to improve customer convenience.