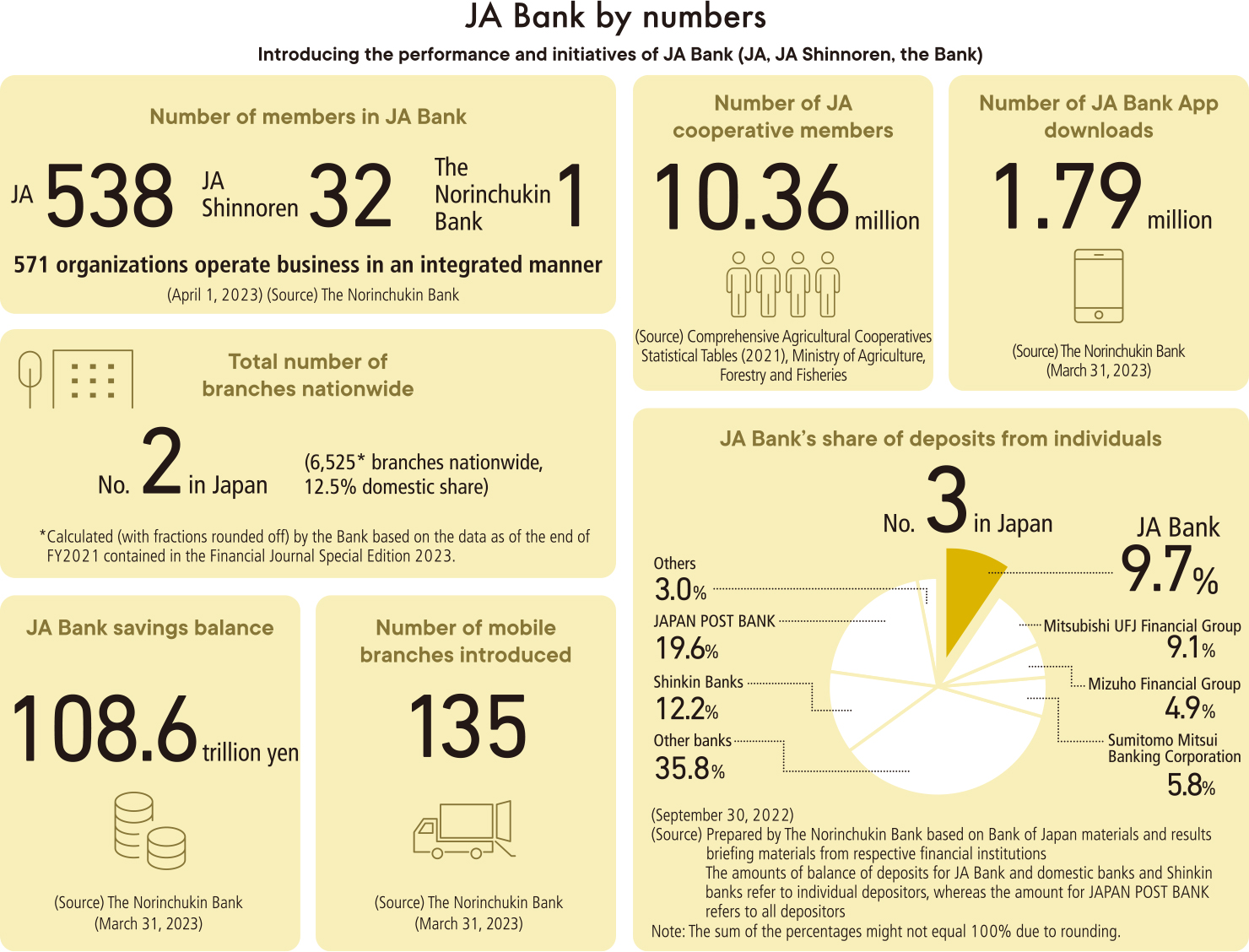

![]()

![]()

Providing a range of financial functions as a member of JA Bank and JF Marine Bank

JA Bank not only provides agricultural loans to support farmers but also offers various financial products and services tailored to the life events of its members and users. In addition to its range of financial services, including savings, settlements, and loans, it also provides investment and testamentary trust services.

JF Marine Bank aims to maintain strong trust and to continue providing essential banking services as the financial institution most accessible to fishery communities. In addition to leveraging its expertise as a financial institution specializing in the fishing industry to provide suitable funding solutions, JF Marine Bank addresses various challenges faced by fishery-related operations, thereby supporting both the fishing industry and local communities.

As a member of JA Bank and JF Marine Bank, the Bank is responsible for formulating overall strategy, and planning products and services. It also works with JA, JF, JA Shinnoren, and JF Shingyoren to consider and implement ways to promote our products and services to our members and users.

KAWATA Junji

Director and Senior Managing Executive Officer

(in charge of Retail Banking Business)

Member of the Board of Directors

Head of JA and JF Business Support

What is the Retail Business?

Our Retail Business is a domain responsible for the following major roles as the national-level organization of JA Bank and JF Marine Bank.

Approach to Achieving Medium-Term Vision

Business Environment Outlook for 2030 (Retail Business)

- As the business foundations of JA and JF change due to such factors as population decline and societal aging, the need for further management efficiency and business reform is gaining urgency.

- Japanese population shift from rural to urban areas is accelerating. The social value and expectations placed on JA and JF as the backbone of local economies and infrastructure, through the operation of comprehensive businesses, are increasing as growing interest in AFF industries lead to companies from other industries entering into the sector.

- With the rapid advancement of digital services, for people across all generations online and low cost simple financial transactions tends to become the norm. However, strong demand remains for face-to-face, specialized advisory and consultation services from community-based, trustworthy financial institutions, especially in asset management. Providing such services could become a key competitive advantage for financial institutions who can provide them.

![]()

Approach to achieving our Vision for 2030

We are focusing intently on the use of digital data for sales support and other functions and, thereby, streamline our credit business and provide advanced services to users. In order to maintain the foundation of our business, we must provide value in ways that remains attractive to users and to approach a wide range of users via digital channels.

We are improving the user interface (UI) and user experience (UX) of non-face-to-face channels via such means as collaboration with JA group’s businesses such as Farm Guidance, Marketing/Supplying Division and Mutual Insurance Division. We will further strengthen our current initiatives to improve the management of JA and JF and enhance our ability to propose compelling solutions to users.

Initiatives for fiscal 2024

JA Bank Medium-Term Strategies (Fiscal 2025–2027)

In order to realize the vision of JA Bank, we have formulated the JA Bank Medium-Term Strategies (Fiscal 2025-2027), which defines a strategy for “Strengthening Connections” and “Enhancing Management Policy Comprehensively Across All Businesses." This is designed to enable us to provide services and experiences from the perspective of our members and users and build user touchpoints that integrate the physical and digital domains.

We supported JAs nationwide in their effort to appropriately leverage their financial intermediary functions to meet with local circumstances. This included the development and enhancement of agricultural financing and various loan systems, proposals for asset formation and management, and initiatives for regional revitalization.

Development and expansion of digital infrastructure

To meet growing demand for online transactions, in August 2024 we launched JA Bank App Plus, a new smartphone app featuring functions such as transfers, changes in address and phone number, and more. Used with the JA Bank App, where users can check savings balances, mutual fund balances, and transaction details, the new app enhances the user convenience of managing account information and performing various procedures via smartphone.

JF Marine Bank Medium-Term Strategies (Fiscal 2024–2026)

In its medium-term strategy for the three years from fiscal 2024 to fiscal 2026, JF Marine Bank, as the JF group’s financial institution and the main bank for fishery communities, plays an ongoing role in strengthening the group’s ability to consult on fishery management and provide advisory services in various subject areas, including the conservation of fishing grounds.

We have supported efforts to resolve business challenges, including those related to the management and finance of fishermen and JF, by sharing solutions to various problems at the JF Marine Bank Fisheries Liaison Conference (held regularly and attended by fisheries operators and private companies), and by strengthening cooperation within the entire JF Group.

What is the comprehensive strategy of JA Bank and JF Marine Bank?

JA and JF cooperatives throughout Japan are independent financial institutions that respond to the diverse financial needs of their local communities, members, and users. In order to provide the necessary retail services more efficiently and effectively, JA Shinnoren and JF Shingyoren collaborate at the prefectural level and work with the Bank at the national level to run integrated business operations as JA Bank and JF Marine Bank.

JA Bank and JF Marine Bank develop their integrated business operations by formulating a comprehensive strategy (nationwide strategy) every three years. Based on this plan, each prefecture formulates a prefectural strategy that would fit each regional characteristic.

Current Challenges and Direction of Responses

Current Challenges

- Changes in the business foundation of JA and JF due to the decline in the domestic population and number of producers in agricultural and fishery industries

- Diversifying issues and requirements among individual members and users

- Response to rapidly advancing digital services; streamlining and rationalization of operations

![]()

Direction of Responses

General

- Continued support for the foundation and implementation of JA and JF management strategies as comprehensive business organizations, tailored to regional characteristics; building a sustainable management foundation (visualization and refinement of strategies through communication with JA and JF)

JA Bank

- Develop support services that identify and explore potential needs of members and users by visualizing their management challenges, financial situations, and life events (e.g., promoting in-person transactions through Loan Enhancement Support programs)

- Work to build points of contact with members and users through optimal integration of digital and real, and develop digital infrastructure (e.g., promoting online transactions through improvements to app functionality)

JF Marine Bank

- Strengthen consulting activities with from external experts’ support to help address the challenges and needs of fishermen (e.g., sales channel expansion, business succession, etc.)